GMV Financing

Embedded solution for sellers on your platform.

What is GMV Financing?

Gross Merchandise Value (GMV) financing is our credit solution that allows sellers on your platform to collect instant payment for the goods they have sold for a single upfront fee at checkout. GMV financing allows your sellers to improve their cash flow, restock inventory faster and ultimately increase their stickiness towards your platform.

How Does It Work?

Built for Every Industry

Our GMV Financing solution is tailored to grow business on your platform. It works on any platform where buyers and sellers transact digitally, from fashion and FMCG to supply chain and industrial equipment.

How Does It Benefit Your Platform?

- Grow Your Platform Revenue & Profits - By offering your sellers capital, they can focus on growing their businesses and increasing sales on your platform.

- Attract More Sellers To Your Platform - You gain a competitive advantage over other platforms that don't offer 'GMV Financing Solutions.’

- Increase Seller Loyalty - With better cash flow control, sellers will likely remain committed to selling on your platform.

- Outsource the complexity of loan decisioning - Outsource the entire credit analysis and loan decisioning to industry experts.

Product Construct

At a Glance

- 1–year credit line based on historical sales data and qualitative data such as reviews & ratings on the partner’s platform.

- Credit line subject to annual renewal.

- The seller would be able to perform multiple drawdowns.

- Repayment is made directly from the seller’s platform wallet.

Underlying Product Parameters:

- Linked to recent transactions on your platform.

- Loan Type: Bullet repayment. Principal and fees due on repayment date.

- Max Ticket Size: Typically up to local currency equivalent of US$ 250,000.

- Max Tenure: Customizable for your seller’s needs (e.g., 20/40/60/90 days).

GMV Financing Fees:

- No charge for approving the credit line.

- Risk-based pricing for each seller (up to 2.5% per month).

- Charged upfront and on loan drawdown.

- Late Charges: None.

- Upfront fee increased by 4% p.a. for subsequent drawdowns.

- The fee is deducted from the loan amount, and the net amount is disbursed.

Loan Documentation:

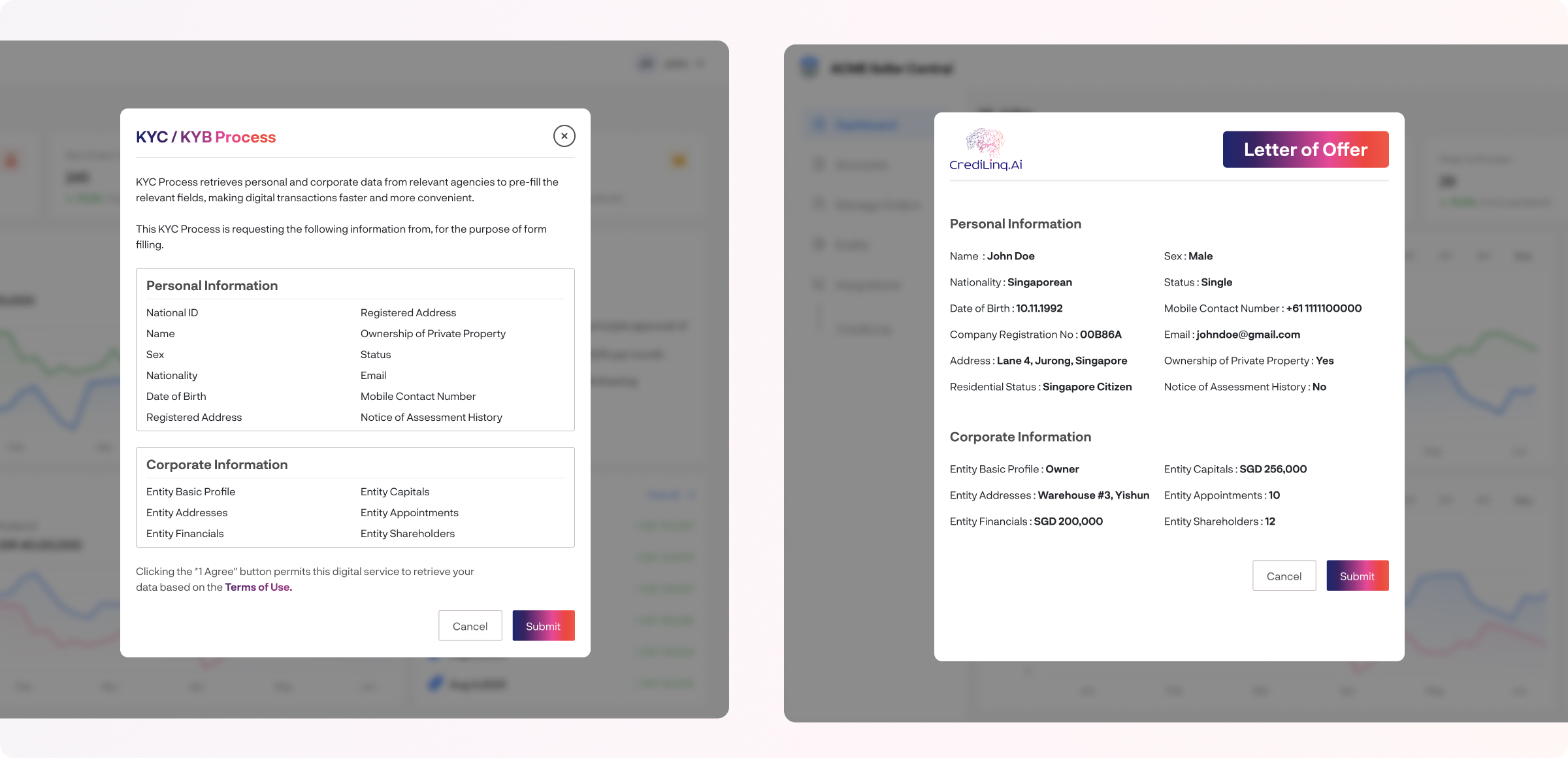

- KYC of seller.

- KYC of individual directors (at least 2).

- Alternative Data: Up to 18 months of the transaction history.

- Loan Documents and Letter of Offer: e-signature integration.

- Access to the company credit bureau (with consent).

Personal Guarantee

No personal guarantee is required for GMV financing.

Loan Monitoring and Renewal

- Daily flow data for sellers to be passed for loan monitoring.

- Ready-to-drawdown limit managed based on business trends.

- Annual renewal with minimal documentation.

Product Workflow

- Seller's dashboard will prompt action to check their eligibility for GMV financing.

- Seller must consent to share their platform data with CrediLinq.

- CrediLinq analyses the data and provides approval in principle.

- We leverage the seller's platform data to pre-populate the Letter of Offer.

- Easily initiate a drawdown from the available credit line.

- Seller's dashboard provides holistic snapshot of available credit line, fees and repayment tenure.

Updated over 1 year ago

Did this page help you?